@itsmect mentioned this too but it is wild how this community just hates cryptpo. There’s a good chance the instance you’re on accepts it for donations. Why would they do that if it is so unusable and bad? Open source everything except the money. Makes no sense.

Haha crypto sux. So funny.

Just don’t ask them to explain why.

Last time I asked, someone explained to me that bitcoin uses more and more power depending on how long the ledger is :)

These pathetic crypto jokes are popular. People adore them. They don’t adore knowledge about even what the basics of crypto are.

Just read an article that said that restrictions in windows 11 will send an estimated 240million PCs to the landfill this year. I bet a lot of people are quick to comment on their Windows PC about how energy intensive and bad bitcoin and other crypto is, though. At least one is doing something that’s never been done before (crypto). I also wonder how much energy it took us to get to the moon? I guess we should have never done that because of the energy it took to accomplish. I wonder if people were like this about vehicles when they were first mass produced and available to everyone.

I don’t even care if someone doesn’t like crypto, I have friends that don’t care for it, but they don’t try to rationalize it with some lame ass arguments that can be debunked by a child. I don’t understand why lemmy is full of these folks.

Yes 😎

Lol I know I hate making money on something and protecting my privacy and data at the same time! How could the “cryptobros” do this to us??

No! It’s all scams and it’s a pyramid scheme! It’s pointless and bad for environment and cryptobros and it can’t work because it’s getting more expensive (literally an argument I heard).

Did you take the decision to comment my meme by yourself or did you have to ask 1000+ strangers to run complicated computations before ?

It’s a brand new shitcoin that uses PoG or Proof of Gullibility. Throw money at the “miners” who do… something then issue you a token that proves you were gullible enough to believe you would make money.

lmao that was good

Did you come up with such a lame joke by yourself or… yes all by yourself, other people would let you embarrass yourself so much.

The only reason the joke might be lame is because it may count as bullying the mentally handicapped at this point

Omg yes, poor mentally handicapped people of crypto lol! With all their money and mathematical equations, inventions, memes,… You really shouldn’t make fun of them or they will cry so much because of you! Oh no! Please don’t make any more jpegs that uncover the worms in your brain. Please no!

Yes, those poor mentally handicapped, whom have such poor social understanding that they do not care about any other being except themselves and their money.

That doesn’t make any sense. You got nothing boy.

Bye.

OK but there are actually great uses for blockchain that are completely disconnected from anything you typically see

For example, banks may begin using blockchain for maintaining their internal ledgers. It will help solve a ton of issues around reconciling the transactions from all over the globe

Blockchain has reasonable uses. Really good ones. Crypto and nft bros just completely ruined the image of it

blockchains do not do jack shit with reconciliating records.

Walmart seems to have had success here, and logistics is their whole thing.

https://hbr.org/2022/01/how-walmart-canada-uses-blockchain-to-solve-supply-chain-challenges

Please go and attempt understanding the thing you are talking about before talking about it.

Blockchain has been around as a technology for nearly two decades. If financial institutions thought it could help them you can bet they would be all-in on it by now. As it is, blockchain has no significant advantages over traditional financial ledger systems, so what incentive is there for them to use it.

It’s not something new or cutting edge any more, just waiting for a bright spark to discover the technology and put it to use.

If financial institutions thought it could help them you can bet they would be all-in on it by now.

Yeah I imagine they probably would.

Maybe do a simple Google search next time? They ARE using it. It’s getting a ton of investment from them.

Also it’s over three decades. Bitcoin wasn’t the first. They just popularized a specific type of blockchain

So much ignorance on display in this thread. Y’all are amazingly confidently incorrect

Maybe do a simple Google search next time?

Rather than resorting to that age-old cry of the cult member “do your own research!” can I respectfully suggest that if you’re aiming to change somebody’s mind, the onus is on you to provide the evidence, not on them. By all means take hours out of your day to search google and compile a list of things that you think will convince me. Me, personally, I have better things to do with my life.

I didn’t ask them to do their own research. I asked that, if they are skeptical of a claim I made, either do a simple Google search to check if it’s very easily verifiable, or ask me directly instead of immediately saying “you’re wrong because I would have heard of it”

Like, I’m happy to provide citations when requested, but lemmy isn’t a scientific journal where I’m expected to provide every source for my information up front

Well, why would banks replace the system which allows them to charge fees for every other interaction with their services? A blockain solution would allow multiple different banks (and, possibly, even regular people) to access the data with no middlemen, and, therefore, no fees. Or, well, no fees that directly end up in the bank’s pockets as profit, that is.

Getting rid of that is bad for business. So, unless something magical happens and the EU, for example, pass a law requiring the banks to switch to a more de-centralized, more fair system, it’s not going to happen.

That’s kind of my point. Blockchain evangelists have been banging the drum for many years saying “This is a perfect fit for the financial industry. Why won’t fintech wake up and recognise that?”

When in fact fintech took a long, hard look at blockchain a long time ago and decided “nope, there’s nothing here that would tempt us” outside of a few very niche applications.

Blockchain is only potentially useful if there’s no single entity that can be trusted. If banks can’t even trust themselves to manage their own internal ledgers, they have much bigger problems to deal with.

Trustless systems aren’t a bad thing that has to step in when the good thing fails. Trustless systems are inherently better because you don’t have to trust a bank (or anyone for that matter).

Additionally, ledgers can be gamed/corrupted/falsified. This is significantly more complex (bordering on impossible) on the blockchain.

Here is an alternative Piped link(s):

https://piped.video/bBC-nXj3Ng4

Piped is a privacy-respecting open-source alternative frontend to YouTube.

I’m open-source; check me out at GitHub.

Cryptocurrency Ledgers can be corrupted?

I was hedging against a particularly snarky commenter showing up. You can do a 51% attack and theoretically corrupt it. In practice, that’s much more difficult.

You dont need 51% attack to corrupt a ledger. Just enter incorrect info and the ledger is wrong. Not a damn thing a blockchain can do about that. Same issue is with any trustless system where you have to trust someone to input the correct info/do the agreed thing/ship the ordered physical item.

Just enter incorrect info and the ledger is wrong.

The concept behind cryptocurrency is that the ledger is the info, because you’re right, a half-assed blockchain ledger used for external (e.g. cash) transactions doesn’t really solve the root problem. Proof of work is fucking stupid though, and it has (rightfully) ruined the perception of blockchain technology among those who can see past their own crypto wallet.

There are often easier, more reliable, and far cheaper ways to achieve the same things without using a blockchain. Some of the principles are even used in normal web browsing to ensure secure untampered connections.

Blockchain just solves a subproblem that only arises when there’s no appointed central entity.

Blockchains aren’t hard, unreliable or expensive

That’s the thing, they shouldn’t trust a single source of assumed truth. If the single source is tampered with, there’s nothing to compare to.

Removing the need to trust a single entity is just a great security feature

If the bank can’t even trust themselves then there’s no point in having the bank at all.

You really don’t get it? Trust is a problem. Anyone, or anything, can and will fail or be compromised.

so I put my trust in software instead. And by extension its developers. You’re saying of all people, we should trust some programmers above all else. You know, the “move fast and break things” guys.

As a programmer myself, this thought is both terrifying and hilarious.

As a fellow programmer: what kind of doomer take is this? I don’t have any opinion on the efficacy of blockchain technology, but all of us put an immeasurable amount of trust in software every single day. And it’s not like current banking practices are different in this regard, either: blockchain tech requires faith in the software implementation, while contemporary banking requires faith in banks and the software they use (including a borderline unmaintainable COBOL stack, from what I’ve heard).

because problems in the bank’s software are the bank’s responsibility. If they lose my money, it’s their responsibility to get it back. Cryptocurrencies are the exact opposite, by design. If you’re fucked, you’ee fucked. unless of course half the participants decide to fork, half don’t and you end up with two “currencies” out of thin air.

Banks and firms that uses their services are audited thoug. It is not blind trust. And regadress the tech used there would sitll be audits.

Blockchains is a tool for moving trust around in a decentralized network, not a tool for removing it.

Security starts with trust.

You can implement public or semi public ledgers without Blockchain. That’s what banks are doing already by sending huge CSV files internally and externally. Blockchain is not a technology of zero trust. It’s close to the opposite. You trust a few peers and blindly trust everyone they trust. That way you trust a network that you know nothing about and if the network decides on a common truth that you are convinced is incorrect, there is nothing you can do about it. The consensus always wins and there is no single entity to complain to and get it fixed. This is great for making sure that many actors need to be bad actors in order to have the whole system fail. It’s bad if you don’t trust anyone and want to make sure that your standards are always observed. From a technology standpoint I love the concept of Blockchain. But use cases that are not forced are few and far apart. Too few for the amount of hype it receives.

i for one would have liked a media licensing system that operates agnostic of any centralized authority

for instance, irrefutable and independently verifiable proof that you own a valid software, music, or visual art license and are therefore immune to prosecution for piracy.

A registry of licenses like this could shield creators from copyright claims on social media applications such as youtube. Could also automate revenue sharing and royalties for artists whose works are used in derivative media so the people who actually perform the work get paid. Would be nice to cut the publisher middleman out. And there is absolutely no reason there has to be anything like a “proof of work” system burning down entire fucking rainforests’ worth of energy to verify every single gods damned transaction because this sort of system isn’t for trading shit, it’s strictly for proving a valid chain of custody between producers and consumers and you don’t need megawatt-hours to just fucking LOOK SOMETHING UP.

imagine if, for instance, fucking warner brothers couldn’t “takes backsies” content that they SOLD to end users through a distribution network; the license is yours, and anyone can look up the fact that the license was sold to the user id you happen to control.

imagine if, for instance, you buy a video game through a digital distributor like steam but then the store goes out of business and no longer exists to serve you a copy or recognize the sale, but on this massively distributed and decentralized database you can prove that you did indeed compensate the developers of that software and thereby legally acquire entitlement to access it in accordance with the end user license agreement.

imagine if ownership of stuff you bought fair and square can never be taken away from you

THAT’S what we could have had

instead of this fucking bullshit.

All such copyright licenses are rooted in local jurisdictional law, so your country’s copyright office should be the authority because anything else means the courts can tell you that your on-chain transactions are invalid

I feel like here you get to the NFT problem of having proof of ownership of something doesn’t mean much when that thing is being hosted on servers you don’t control

so if you have an entry with a licence for a steam game, and steam gets closed, you are out of luck

NFT’s don’t show you have proof of ownership of anything other than the NFT. Think of all the people who got their metamask account hacked and lost all their apes with zero recourse.

Why would anyone want anything required for daily life attached to something so insecure and irreversible as that?

It’s like if losing your wallet automatically burns down your house. Sounds amazing, let’s do it!

imagine if, for instance, you buy a video game through a digital distributor like steam but then the store goes out of business and no longer exists to serve you a copy or recognize the sale, but on this massively distributed and decentralized database you can prove that you did indeed compensate the developers of that software and thereby legally acquire entitlement to access it in accordance with the end user license agreement.

What you’re arguing for is forcing the distributor to distribute in perpetuity, which has nothing to do with how you show ownership of your license.

Right now, I can show steam I’ve purchased, say Delistopolis, and they will agree I am indeed perfectly allowed to have and play it. But they are not required to provide me with a copy.

A blockchain system will not solve this.

no. you’re putting words in my mouth. if the distributor wants to stop distributing they can.

they can take down their servers, they can even cease to be, but it would no longer affect the availability of product they sold.

Then I don’t think I understand you. Are you suggesting we put millions of full games on a bloxkchain?

Only the keys need to be stored cryptographically, really, because the game files themselves are nigh inevitably available on torrenting networks. it’s inevitable that people are going to rip backups of all game files for the delicious delights of datamining and as long as enough of them will seed them (which shouldn’t be a problem as long as there’s any INTEREST in a game existing…) that availability never arises as an issue. And if it’s not popular enough to put there, it’ll probably end up on The Internet Archive.

Would be nice if there were an infrastructural ‘backup of last resort’ such as the library of congress, which is something the LoC already does for other audiovisual media. It’d just be nice if that service were extended to software.

Well, if those licenses are entries on the blockchain, they could be transferred on the blockchain. You could sell your game used when you’re bored of playing it. You can’t play it after you sell it but someone else can. Publishers hate resale markets though, when people buy used games they don’t make any money. So they’ll probably never go for this.

yeah on top of that, if your computer breaks or something now you lost all of your keys.

say goodbye to whatever you own on the blockchain when the keys are gone. poof!

this is the biggest problem with any scheme tying private keys (digital) to anything in the real world.

Once my mom threw out ask the cases for my computer games and put all the disks into a cd binder to save room.

It was devastating.

She wanted you to hear some of her favorite chiptunes but she didn’t know how

I don’t know what this means

Serial key generators would play chiptunes in the background - give a listen!

Not really. You backup you keys like a normal human. Or create any of those new account abstraction keys that are tied to another account, or anything else.

Not really. You backup you keys like a normal human. Or create any of those new account abstraction keys that are tied to another account, or anything else.

With smart contracts on blockchain you can do exactly that. Everyone involved in the process can ensure they get their cut.

Why would you want the computational power of a bank system have anything to do with whether it’s ledger is correct?

Banks/hackers can manipulate data if they want to. Manipulating data on blockchains is way waaaaay harder.

Using a blockchain to maintain their internal ledgers means they have complete control over that blockchain, so they can manipulate it all they want. Blockchains aren’t magic.

Oh, didn’t see the “internal”. Yea, that’s stupid then.

Who are “they” in the above message?

If you trust all your employees then an internal blockchain is useless, but do banks really totally trust their employees?

A blockchain won’t solve incorrect transaction information any more than an audit log in this case. This is an entirely internal process controlled by the bank and access would be restricted, so they couldn’t just edit audit logs. How do you think a blockchain would be used to improve this?

The actions that an employee could perform would be limited by their private key’s abilities. Blockchain can be preventative. It’s not only for retrospective analysis.

The actions that an employee could perform in any database would be limited by their account permissions. Blockchain doesn’t change this. I pointed out a retrospective mechanism because a completely internal blockchain wouldn’t prevent tampering either.

Yeah let’s use the computing power of an entire country to pay for a small coffee.

you’ve just demonstrated your lack of depth of understanding of blockchains. congratulations, your opinion was correct about 15 years ago. the technology has moved on

You say so but I guess it’s hard to convince a lot of people who recognize it’s folly to try to fix a social/human problem with a technological solution.

Git is a merkle-tree based system like a blockchain. People have no problem with the tech. They’re just tired of the hype train.

and the “solutions” are all objectively worse security wise. And by thinking blockchains need proof of anything, you too misunderstand what a blockchain even is. Proof of whatever is needed by the concensus algorithm, not the blockchain.

no; they all have trade-offs and that’s different… you can have trust less proof amongst semi-trusted parties like a consortium of banks: they don’t entirely trust each other, but trust each other enough to keep an eye on the other members of the consortium

there are plenty of situations like this that are non-public

they are objectively, mathematically weaker.

Joining ethereum now implies trusting a complete stranger to get you up to speed. It is objectively subjective.

i wasn’t talking about ethereum, and i don’t think anyone was saying they don’t have TRADE OFFS. in the world of consensus protocols, there are many different trade offs that build a network that suits your needs

however the consensus protocol has little to do with how mathematically secure a network is: the security of the consensus protocol comes down to a lot of complex things

it also has nothing to do with how you bootstrap a node

these things are all different, albeit interconnected things

the consensus algorithm is the only thing that contributes to the network’s security. That, and because it’s trying to solve an impossible problem, it also needs the psychological element exploiting humans’ greed (and therefore want to hoard currency).

While that is an inherent component of how proof-of-work cryptos work, and utterly stupid, it’s not an inherent part of how to do blockchains.

You can have a blockchain without consuming stupid amounts of energy.

Yeah it’s called a database…

There aren’t a lot of distributed databases with no single owner and all writes are signed.

Yeah, but not having an owner is actually a fucking terrible thing for a banking system, how do you not grasp this?

No owner is great for a banking system. It stops the owner printing money whenever they feel like it.

Bruh

I do grasp it.

I don’t really know what situation it makes sense for. It seems like a tool for cases where nobody can agree who should own the records of something so now everyone should.

exactly, you have others methods of proof-of-work

How is the blockchain different from a read only ( write only once to be specific) DB that follows ACID?

Replication and verifiable timestamps, which you can add to regular databases too BTW

How can you trust that the database is really append only? Blockchain provides a way to verify the state of the database and the ordering of the transactions. Beyond that, not much benefit to be had. However, for certain situations, that is a very big benefit!

Name fucking one situation

Sure! So some students of mine were working on a multiplayer video game that was started by a different group of students the previous semester. The first group of students made a design choice that, to over-simplify, basically tracked achievements and milestones on the client side and then synchronized those achievements to the server. Players could cheat the system by sending malicious packets of achievements to the server. Some achievements could only be completed by a single person in the game, so this was a big problem for the 2nd group of students to overcome. Faced with the choice of rearchitecting the game to be more authoritative on the server and less resilient to frequent disconnections, which affected some aspects of the game, or creating a logical and verifiable sequence of in-game events on the server side. The students went with the latter, and implemented a Lamport clock using a blockchain to verify the authenticity of the events, and prevent a rogue student from updating the game later to give themself a bonus. Basically, along with needing an authoritative sequence of events that is protected from user interference, it also needed to be protected from developer interference.

It was kinda similar to that situation a few years back of the EVE online developers playing the game and giving their guild members certain bonuses and special in-game items. The solution there was to fire the malicious developers, but I can’t exactly fire an entire class of students from an educational project.

To your edit; it was a great example, but if you say anything positive about blockchain (or Apple, or capitalism, etc) you’ll likely be heavily downvoted on Lemmy.

Yeah, I think that seems to be the case here. It just feels to weird me to have a politicized data structure.

“Remember kids, only coke-fiends and meth-heads use Binomial Heaps.”

It’s distributed so no single entity can take it down. Among many other possible benefits depending on architecture and infrastructure.

It’s far more complex than coins and NFTs. Blockchain is like a new internet. Coins and NFTs are like those shitty GIFs you used to see everywhere. Evocative of old internet, but not the internet itself.

How is that useful in a bank ledger?

Simple, it’s not. If it were, they’d have been using them for decades (blockchains were invented in the 70s).

The consensus algorithm, which is not the blockchain itself, was invented later. But banks don’t need to reach concensus with themselves. They all maintain their own data, and heavily guard it. So the only bad actor they could have is themselves. And they banks all keep watch each other.

Preaching to the choir here.

Distributed databases have existed for decades. It’s how large healthcare systems maintain electronic health records for their patients across dozens of hospitals in real time.

This isn’t true: there are not-distributed blockchains.

The definition of a blockchain is a ledger where every entry is cryptographically signed with a hash of the current entry plus a previous entry. There’s no requirement that this be at all distributed. In fact, QLDB uses a non-distributed blockchain as its audit log.

Blockchain are often used in distributed systems because of the verifiability of the records; its a way of providing security of history in a fundamentally insecure environment. But there’s no requirement that they be distributed, and they add value in non-distributed environments as well - in any case you want to be able to review a history of changes and know that someone hasn’t been cooking the books, for instance.

I’ll give a real-world example. One place I worked we had databases that had data constantly streaming in from many different sources. Something that would frequently happen would be some data issue that would break applications; often, this was bad data from sources outside of our control. OPs, who’s only priority was to get the applications back up and running, would often track down and directly modify records and fix the data. The issue was that some time later, sometime days later, a customer would call and complain about data being incorrect. By then, it was impossible to figure out what had happened: did we get the wrong data from the source? Did one of the import processes mangle the data? Did someone poke around in the database and change the data? We had no way of telling, and investigations would take many hours, often from several senior people, who would frequently in the end have to shrug and say, “we don’t know.” There were lots of things that could have improved this, with varying levels of success, but a global audit log would have been the first step. A verifiable audit log would have been better, because often it’d come down to us being convinced the data a third party was giving us was bad, and it became an our word vs. their word since we shared the same client. If we’d had a blockchain layer through which every transaction was recorded, we could have rolled back in time and figure out exactly how a record came to be what it was and been able to prove it to the client.

Blockchains are awesome. People who say otherwise have their heads up their asses, and are unable to differentiate between blockchain the technology, and the sometimes questionable uses they’re put to. Iron is used to make guns and bombs; that doesn’t make iron bad.

Thank you for being in this thread. I felt like I was taking crazy pills with all these other replies. So many people think bitcoin was the first blockchain. And that the paradigm used by crypto is the only type of blockchain there is.

I will never forgive tech bros for making blockchain a buzzword tied exclusively to crypto and NFTs. The amount of lost potential is infuriating

It’s become one of my pet peeves.

I have a conspiracy theory that a lot of the anti-cryptocoin stuff that gets posted is an organized disinformation campaign run by some governments and central banks who are particularly threatened by crypto, and that it extends to bad-mouthing any technology related to cryptocoins. I also believe that there are a fair number of secondary internet users who read “crypto bad” and have picked up the messaging because (a) they’re kinda pissed they didn’t get in on the ground floor, (b) they lost money playing in the markets, © because, whether they’re self-aware enough to know it or not, people love a good mob mentality, and/or_ © because crypto farms really are shitty wastes of resources and are easily villified. I guarantee, however, that not a single one of those people could describe - in even then most general terms - how a blockchain works. Not even at a programmer level, although the programmers who do this are the worst, because they should know better. And this is what infuriates me: “Blockchain is bad!” “Why?” “Because I read it on the interwebs that it causes global warming and is a pyramid scheme!”

Pet peeve.

What do you have against bombs?!

Very interesting perspective, thanks :)

Blockchains add cryptographic signing and limit actions based on those signatures.

Big words that mean nothing

To you maybe. Maybe other lemmings reading this understand them.

They mean nothing in the sense its nothing you cant do with DBs, so like I said, big words that mean nothing

Cryptography - means that only you can make changes. No database administrator. No hacker. No-one but you.

Limited actions - means the changes you make must follow rules that cannot be altered by anyone.

Both impossible to implement on a normal DB, which is why bitcoin was revolutionary.

-

thats not what cryptography means, and is a huge fucking downside especially for banking which us centrally controlled

-

It’s called triggers, user roles etc, once again you dont want this to be unalterabale for banking because what if regulations change…

Only thing bitcoin revolutionized was the speed with which scammers can dupe people out of their money.

-

I love how you can’t provide even a single example of useful Blockchain functionality. Doesn’t mean it didn’t exist, but says something… And no, “banking” and “internal ledgers” is not detailed enough to be a sufficient example.

How about Git?

You just… linked your own comment. I mean, most of us are nerds, but can you just… use language? What benefit does it provide?

I linked you to my other comment where I provide FIVE links to the thing you said I “can’t provide”. I had literally already provided it elsewhere. So that’s where I sent you. Excuse me for not retyping the same thing for every single person.

I don’t owe you my time. I provided a one-click path to what you asked for but you couldn’t even be assed to ponder why I linked you that comment.

Done with you now.

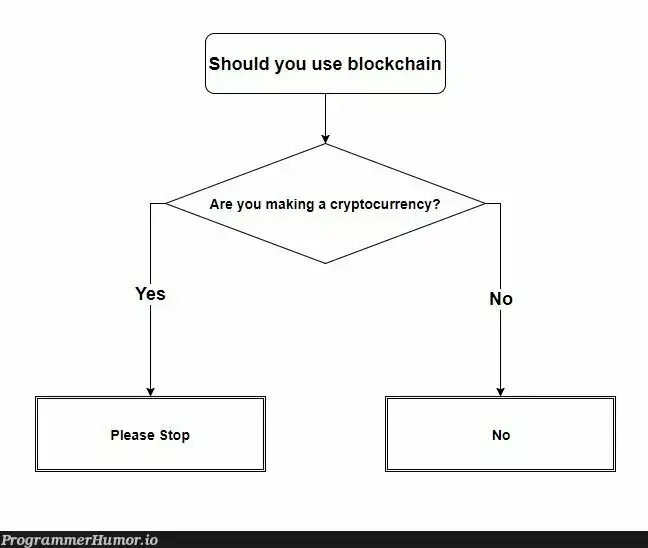

How do you see memes like this? Because I see them as lame and sad, especially since we have been seeing them for 10+ years now and they are still the same. But apparently you think blockchain has reasonable uses.

Misguided

Only misguided?

I mean usually they are accompanied by false information and references to stuff like “crypto bros”, “pyramid schemes”,…

You said “memes like this”. This one I see as misguided. Ones that shit on crypto and nft I generally agree with.

This one is shitting on crypto.

No, it’s shitting on blockchain too. The only options are “don’t use blockchain” and “stop making crypto” which is misguided. I agree with the sentiment about crypto, not about blockchain

There is no blockchain without crypto.

Damn! You had my up vote until that last sentence.

Why? He used the same exact words?

Because I agree with everything except the last sentence. Even after a decade the thinks the block chain has no uses.

He literally said he thinks it has uses.

I think he is most certainly right. People that think otherwise should go back to their bar order another one and keep ranting about it to their half dead drunkard friends.

No, he said “you [meaning in contrast to himself] think it has uses”

As a bitcoiner I couldn’t agree more, please don’t make another cryptocurrency.

You mean like one with actual practical value, one you can program, do actual finance with?

This is how tech people often think because they don’t understand economics and the value bitcoin provides. Bitcoin was distributed fairly, is stable, is scarce, and most importantly, is decentralized. Probably all “programmable” shitcoins have zero of those properties and the market reflects that.

I don’t even know where to begin. Btc was distrubuted as fairly as anything else, it’s not as stable as since we have stablecoins, scarcity means nothing, it’s decentralised as much as anything else.

Must I repeat that it just exists? You can’t do anything with it. It’s like comparing a pretty rock to a computer. Today all what btc does is pollute.

Btc was distrubuted as fairly as anything else

Ever heard of ethereum premining? Or which programmable shitcoin are you talking about?

it’s not as stable as since we have stablecoins

Ouch, fiat thinking. Bitcoin has a stable issuance schedule (changed over and over in eth for example), that’s what I’m talking about.

scarcity means nothing

Like I said, you don’t understand money or economics. Aristotle already knew that money has to be scarce.

it’s decentralised as much as anything else

I guess your dear leader Vitalik doesn’t exist. Or, again, which shitcoin?

Today all what btc does is pollute.

Haha, at least now I know you’re a proof of stake shitcoiner. Probably eth. Proof of work solved a problem proof of stake doesn’t: trustlessness.

You can’t do anything with it.

You know which currency you can do by far the most with? The USD. Are you bullish on that?

we need the blockchainsaw

I’m kinda amazed I haven’t seen anyone mention the biggest upcoming use case for block chain here. In a world where anyone can create any media with Ai we are going to need robust systems of cryptographic proof of origin and history that anyone can access and that is not controlled by anyone who may wish to manipulate information. The exact strength of block chain.

As for cryptocurrency I’m seeing a lot of confusion here in how people think it works. While scaling has been an issue its not an insolvable one and multiple solutions exist. The issue with crypto is its image not the tech in general. And thats a combination of people using it to scam and governments/banks doing their best to discredit it.

I’ll likely get downvoted but Polestar, the EV automaker that used to build performance variants for Volvo, uses blockchain to track minerals used in their EV’s.

Circulor Circulor’s blockchain technology enables tracing of extracted raw materials, particularly those with significant impact to communities and the environment.

I like that they use blockchain to ensure the minerals they use aren’t coming from negative sources but I’m sure someone will argue and say it’s stupid or that SQL can do the same.

git is a blockchain, just without PoW

You can use blockchain technology for a wide variety of things, just please more cryptocurrency and NFTs.

Nothing particularly useful though. It’s a very slow, inefficient, trustless, immutable database. There really aren’t many good applications for that.

That highly depends on what blockchain implementation is being used and what it’s being used for. Blockchains used for craptocurrency are highly inefficient, which is the vast majority. But there are a small handful of specialized (proprietary) blockchains that are just efficient enough to be practical in their highly specific use case.

Such as?

Walmarts proprietary food tracking system based on Hyperledger Fabric that they partnered with IBM to tweak & implement, enabling customers to track ingredients back to the farms within seconds, improving food safety and optimizing supply chain operations.

How is that better than a database? Is someone concerned that Walmart will fabricate supply chain tracking?

Their prior database lacked transparency, real-time tracking, & scalability making tracing take days.

Just an FYI, Hyperledger Fabric is not like the blockchains for craptocurrency. It’s a highly modular, permissioned not permissionless, distributed ledger & it allows for pluggable consensus mechanisms. It’s very likely that Walmart uses a custom consensus algorithm and nothing like any of the public PoW, PoS, or PoA consensus algorithms.Interesting! Thanks for elaborating.

Hyperledger is just git but with fancy buzzwords. It’s like taking everything that makes blockchain, and then remove everything that makes blockchain special. All you have left is another centralized system.

It’s just IBM’s excuse to stay relevant.

That’s an incredibly wrong oversimplification.

Git doesn’t have any consensus mechanisms, chaincode execution or ledger, is just a history tracker & manipulator. Neither Git or Hyperledger Fabric are centralized, they’re both distributed.

Just because it’s for specialized non-financial related tasks using customizable specialized consensus mechanisms and often distributed only within a select few instead of being a big inefficient permissionless PoW/PoS craptocurrency blockchain with a bunch of clowns waisting energy mining nonsense doesn’t make it any less of a blockchain with smartcontacts and the works.with fancy buzzwords

That’s literally just all blockchain technology ever.

“Just blast them with buzzwords they don’t understand to distract from how fundamentally flawed our shit is and FOMO the shit out of them then rug pull every last dime from them” - NFTs.Git doesn’t need consensus mechanisms because it’s “permissioned”, like Hyperledger. All actors are known and given permission by some entity to contribute.

You can’t contribute to the Linux kernel unless your changes have been approved by someone trusted with permission. You cannot contribute to whatever Walmart is doing, because you haven’t acquired permission to do so.

I’ve read through this whole thread, and I still haven’t really come to any solid conclusions on it. I’m skeptical of crypto as a kind of idiotic speculative market, but that’s also every market ever. But then, the blockchain is apparently different from crypto, even though they’re both hype-laden marketing terms that have been completely fucked up. I think doing [redacted] with crypto is still potentially cool, though I think it still has limited anonymity, from what I’ve heard, and the speculative market also fucks it up.

Is “the blockchain” just like some nerd shit that’s for internal hospital ledgers, and beyond that it’s all kind of moot garbage, or what? Someone spoonfeed me.

So data stores tend to present interfaces which allow the CRUD operations on each record: Create, Read, Update, and Destroy.

Create: You hit submit on a comment form Read: Your client app shows the content of the comment Update: You hit submit on the comment editing form Destroy: You delete the comment

Well, in some cases it’s very handy to make a data store with only two operations: Create, and Read.

This is called a “log”. A log is an append-only data structure.

One of the benefits of using a log is that two different processes can operate on the data, at different times, and can be confident they’re operating on the same context despite not being in communication with each other.

This “log” structure could be useful for instance in recording the moves of a chess game. Then, a hundred years later, someone can read each move out of a book and deterministically re-create the board state.

Now they know that they are looking at the same chess game that Ben Franklin was in 1775, despite not being in touch with Ben at all.

Really big, distributed systems benefit from this “synchronization without communication” feature of logs.

Excellent article on this data structure and its benefits here: https://engineering.linkedin.com/distributed-systems/log-what-every-software-engineer-should-know-about-real-time-datas-unifying

Blockchain is a log.

Relying on a log requires you to trust that nobody else has Update or Destroy access. For it to work correctly and everyone be on the same page, Updates and Destroys need to never happen.

With a coordinated system like people trying to understand historical chess games, or a corporation like LinkedIn seeking its own self interest, there’s no trust issue.

But with other things, like “who’s got how much money”, people don’t want to have to trust that some centralized log owner is modifying the data on the sly.

That’s where blockchain goes beyond a regular log. It’s a log designed to resist tampering, because each “block” in the chain goes through a distributed checking process where many copies of the log are used, and everyone checks each other’s copies to ensure nobody is cheating.

It’s the whole web 3 concept of the community powers the infrastructure to run the community. It’s an enticing concept, The people using the service pay with their CPU and internet connection to use the service. It makes what would be a rather expensive infrastructure almost free.

With blockchain they’re doing some smart things, you can wrap code around the ledgers, in the end it’s just varying fancy levels of receipts verified and secured by the community. It’s verifiable but anonymous.

But then you’ve got cryptocurrency doing complex math burning through tons of electricity looking for unicorns to add to the ledger, in a massive pyramid scheme. Okay, it’s not exactly a pyramid scheme. Whoever starts a given currency makes the vast majority of the money off of it when the coins are easy to find, but at some point it is pretty close to any other given financial system, with the benefits of being anonymous and verifiable.

The bitcoins are just entries on the ledgers. But then s*** like NFTs are on ledgers. Someone sells you a receipt for a JPEG on a URL. It’s all only worth what someone will pay you for it. And without a whole bunch of regulation, it’s not exactly a safe market.

One is the tech, the other is an example of a type of the tech. A square is a rectangle, but a rectangle is not a square.

For most applications, this isn’t necessary:

There are some examples like in biotech/finance that I personally believe will require a blockchain to be truly “fair” at the end

I like this flowchart but honestly most third party data handling solutions are just asking for a major breach: stoking vulnerable people over the coals.

Diagram is missing a “do records need to interact” control box.

Now add that trustlessness is impossible and you can scratch the blockchain box for good.

You cannot get rid of trust in some form. You need entry to the system, so you need to trust its gateway. You need to trust the network to not have some vulnerability like a 50% attack. And eventually you need to trust the developers not to add critical bugs (that alone is virtually impossible) or pull off some scam.

So, since you need to trust someone, might as well choose some government regulated party like a bank or a lawyer and choose conventional and efficient tech.

I’m stupid, can you give me a like, more clear practical example of a good use of blockchain? Cause I get the sense that a good amount of this conflict, going off that flowchart, is going to be due to the evaluation of these situations as like, not needing to arise in the first place, or maybe like, a philosophical objection to the necessity of the technology, maybe. But I think a clearer example could help with this.

A blockchain can provide an irrevocable record, and it can provide a mechanism for uncooperating parties to agree that the record should be created. This is usually used for financial transactions involving coins of dubious value, but it can also be used for recording transactions of real world assets as long as those transactions can be faithfully linked to the event on the blockchain. Therefore the blockchain doesn’t really prove that a transaction is fraudulent or not, all it proves is that a sufficient number of parties believe it is not.

as long as those transactions can be faithfully linked to the event on the blockchain.

That kind of seems like the big glaring video game boss style weak point, to me. I feel like you’d still need some external third party to verify that everything is properly linked up to the blockchain, or like, someone could just impersonate someone else through whatever things are used to link something to the blockchain, and then it’s just kinda back to square one, I would think. I dunno, I think also maybe I just don’t really quite get it.

The blockchain is essentially a ledger that tracks transactions (including the creation of currency). One thing that is not always clear is how important it is for a blockchain to be decentralized. When I say “decentralized,” I mean that many different people are operating a server that performs transactions on a larger network. These people are rewarded in currency for their efforts, and are sometimes referred to as “miners,” though this term is changing somewhat.

There are thousands of these servers in a network that are operating on and tracking the ledger for blockchains like Bitcoin or Ethereum. Any updates to the ledger are verified by all of these nodes. As long as 51% of nodes can verify a transaction, it will be added to the ledger. This means that as long as someone doesn’t own 51% of the network, they can’t just inject whatever transactions they want (i.e., fraudulent activity). In practice, this makes these networks very resilient to fraud.

I think this paves the way for a lot of the practical examples you’re looking for. For example, there’s no way for the network to decide to just give tons of money to a single entity for some “economic policy” like Too Big to Fail (i.e., corporate bailouts). This means you don’t have to wake up one morning worrying about whether or not your currency will rapidly inflate because of things like corruption. Another example is the true ownership of digital assets. NFTs have (rightly) gotten a lot of flack for being overpriced JPEGs, but there are real use cases here. A random middleman can’t just decide to price gouge because they own all the tickets first (Ticketmaster). Instead, artists can mint tickets on the blockchain (very important: this ensures authenticity) and then fans can buy them on the blockchain - no middle man required. You still show a QR code at the door for verification like you would now.

As long as 51% of nodes can verify a transaction, it will be added to the ledger. This means that as long as someone doesn’t own 51% of the network, they can’t just inject whatever transactions they want (i.e., fraudulent activity). In practice, this makes these networks very resilient to fraud.

Could like, 51% of the owners just coordinate to kind of, do a fraud? I mean it sounds like an inherently democratic system, but from what I’ve understood of, say, miners, right (dunno how this works for proof of stake, but I imagine it has similar problems), those rigs are gonna be bought by people who disproportionately have higher earnings and can afford more GPUs in finland or wherever, and then that’s going to just kinda recreate the same power dynamic that we see in the real world already. Which ends up in the same kind of speculative market garbage we have with stock ownership in companies already.

I also don’t really understand how a ticketing system would really work on the blockchain. I probably don’t know enough about cryptography to know how it might work, but I got the sense that nfts weren’t even overpriced jpegs, they were overpriced links with pseudo-legal contracts, that were still prone to link rot, and didn’t really indicate any IP ownership. If you had a code on the ticket instead that could only be verified as real, rather than fake, by a ticketing person, instead of like, a link, that would probably be the use case, right? am I getting that correct, is that something cryptography can do? probably, right?

Also, can someone just like, steal your ticket still? Or like impersonate you as the ticket guy, or what? Like from the others have told me and also just from what I know already, you can’t really change the chain unless, like you said, you have 51% of the owners, so how would you be able to like, put something in the chain that identifies the owner as being the owner? Wouldn’t it be more secure to have just like, a verifiable code or something, that you can delete, that isn’t public, between the artist and the buyer? Then you could ensure anonymity between the buyer and the venue and stuff, you could work in establishing characteristics like oh here’s my driver’s license, here’s my government ID, without putting that stuff on the blockchain, which seems like a bad idea.

In practice, this makes these networks very resilient to fraud.

Could like, 51% of the owners just coordinate to kind of, do a fraud?

Sybil attacks sound like the kind of thing you’re talking about. I don’t have the expertise to go into it, but one person (or a group) creates lots of nodes and uses that influence to do bad things to the network, potentially including fraud. Or as you suggest, legitimate users can just coordinate to do whatever they wanted (see ethereum vs ethereum classic if you want a chuckle).

I want to make a note that the networks are only resilient to a specific type of fraud - people trying to enter data in a way that doesn’t meet the criteria of the system. That’s all well and good for wallet to wallet transactions, but when you have transactions going off chain (like buying something, trading for other kinds of coins, doing anything with crypto exchanges), there are still plenty of other kinds of fraud that are possible and happen all the time, because while the chain is fairly trustworthy, nothing else about the system is. Most kinds of fraud involve doing things that technically you have permission to do, because you lied to people to access their password or promised them bigger returns in the future or missold a product or service etc and all of that is still possible under crypto. In some cases crypto is more vulnerable to these things because of having no central authority or regulator or laws or whatever.

Blockchain technology can improve health care services in a decentralized, tamper-proof, transparent, and secure manner.

This can also be used for research institutes to be able to research with each others’ findings.

Here is a paper on the topic: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8555946/

Blockchains are also great for the verification of digital goods as tangible assets. While I’m not sure we reach this level of meme, people could 100% mint their own house’s deed and trade that as a legit way to buy/sell their house.

I am very carefully avoiding the words “NFT” because they are another horrible use-case of a blockchain (and a prime example of how capitalists turn a good tech into something stupid for a quick buck), but this would theoretically be a tokenized-security with a 1:1 to the actual deed to the house.

Is that more secure than the normal process of buying a house? Do you really need it to be external to a 3rd party when the transfer of homes already exists? No not really lol, hence why we probably see it the most in highly regulated industries like biotech and finance first.

HIPPA/Securities-laws (or lack-thereof) will require a tough regulatory framework that “could” realistically be done via a 3rd party, but you have to ask yourself if you trust big-pharma and wallstreet enough to regulate themselves like that.

Edit: Looked up and saw c/lemmyshitpost, maybe I’m spending too much time elucidating a response on a meme thread but this is my take on the tech.

No no, thank you for this.

I understand blockchain as a concept, and kind of hownit plays into cryptocurrency, but understanding a true example of blockchain use outside of finances is something I needed more info on, thank you

The big improvement is the removal of the need to trust some 3rd party but also to add the precision and complexity of computer language to some domain. For example health care data, a block chain system would make one standard for how the records are stored, it would make it so the data in encrypted by the patient and they alone could grant access. When a new provider wants access there is one standard way that is automated and secure. None of which is dependent on a 3rd party who can be compromised or become corrupt and no longer act in good faith. Obviously there is a lot of details here dependent on making the block chain work flawlessly.

Imo block chains have 2 core issues to over come in order to really solve problems. First is being constructed so that they are bug free. Software is not a mature enough discipline for that as of yet. Second, is what happens when you loose you key or it gets stolen. If someone steals you Bitcoin private key, you can’t get them back after they transfer them out. Or if you just loose the key your up a creek. What is required is a way to prove you are you to the system that can’t be stolen and can’t be lost. That is a far harder question.

I just wrote out another comment, and I think I kinda figured out my core question, but, is there a way to save my medical information without doxxing myself, if this is supposed to be like, a public database, you know, if that’s kinda the point, is that everyone can look at everyone else’s stuff? I got the impression that a lot of the current blockchain stuff wasn’t capable of the necessary levels of storage that would be required for like, health records, on their own.

I dunno, maybe you could have some situation where you have a key, that opens up some cryptography on the blockchain, and that blockchain piece when unlocked gives you another key that lets you access your medical records, or something like that, and that might be able to fit. But, then, I don’t really see how that’s any different from just having like, the key to the person’s medical records be contingent on person. Like biometric security, or government ID, or something.

Point out wherever I’ve made wrong assumptions here, I’m just kind of talking out my ass, and hoping that I’m correct inso that the conversation can continue and I can scrape more out of it, I don’t really expect to be right.

can you give me a like, more clear practical example of a good use of blockchain?

Do you see how all the answers are generic, tend to be long and read like a sales pitch? That’s because the actual answer is: no, there is no practical legal application that isn’t better solved with conventional tech.

The only application that is successfully used in practice is paying for organized crime: buying goods and services on the dark web and paying for extortion like ransomware attacks.

Git is not a blockchain. There is no distributed ledger; no consensus algorithm.

Ledger: repository database.

Consensus algorithm: repository access key.

A blockchain is just an verifiable chain of transactions using cryptography and some agreed upon protocol. Each “block” in the chain is a block of data that follows a format specified by the protocol. The protocol also decides who can push blocks and how to verify a block is valid. The advantages it has comes from the fact the protocol can describe a method of giving authority across a pool of untrusted third parties, while still making sure none of them can cheat. Currently the most popular forms are Proof of Work (PoW) and Proof of Stake (PoS).

Bitcoin for example is just an outgoing transaction to a specific crypto key (which is similar to a checking account) as a reward for “mining” the block, followed by a list of transactions going from a specific account to another account. These are verified by needing a special chunk of data that turns the overall hash of the entire block to a binary chunk containing a number of 0 bits in front, which makes it hard to compute and a race to get the right input data. This way of establishing an authority is called Proof of Work, and whoever is first and gets their block across the network faster wins. Other cryptocurrencies like Ethereum use Proof of Stake where you “stake” currency you’ve already acquired as a promise that you won’t cheat, and if someone can prove you cheated your stake is lost.

The problem it solves is not needing a trusted third party to handle this process, such as a government agency or an organization. Everyone can verify the integrity of a blockchain by using the protocol and going over each block, making sure the data follows the rules. This blockchain is distributed so everyone can make sure they are on the same chain, else it’s considered a “forked” chain and will migrate back to the point of consensus. This can be useful for situations where the incentive to cheat the system for monetary or political gain outweigh the cost of running a distributed ledger. It can also be useful when you don’t want anyone selectively removing past data as the chain of verifiability will be broken. The only issue with this is you need some way to reach a consensus of who gets to make each block in the chain, as someone need to be the authority for that instant in time. This is where the requirement of Proof of Work (PoS) or Proof of Stake (PoS) come in. Without these or another system that distributes the authority to create blocks, you lose the power of the blockchain.

Examples I’ve heard of are tracking shipments or parts (similar to how the FAA already mandates part traceability) and medical records. This way lots of organizations can publish records relating to these to a central system that isn’t under any single entities control, and can’t change their records to suit their needs.

These systems are not fool proof though, PoW has the ability to be abused using a 51% attack and PoS requires some form of punishment for trying to cheat the system (in cryptocurrency you “stake” currency and lose it if you try to cheat the system). Both of these run into issues when there is no incentive to invest resources into the system, a lack of distribution across independent parties, or one party has sufficient power to gain a majority control of the network.

Overall you are right to be skeptical of cryptocurrency, it’s been a long time since I participated due to the waves of scam coins and general focus on illegal activities such as gambling. The lack of central authorities also perpetuates the problem of cryptoscams, as anyone can start one and there are limited controls over stopping such scams. This is not dissimilar to previous investment scams though, it’s just the modern iteration of such scams. The real question is does it solve a real problem, as Bitcoin did in the sense it helps facilitate transactions outside of government controls. You might not agree with that but it does give it an intrinsic value to a large number of people looking to move currency without as much paperwork. Now if it makes it worth $68.5k USD (at current prices) is a different story, different people have different use cases and I only highlighted one of those.

The cryptography has much simpler algebraic analogues - what we are looking for is a “one-way function”. This means a mathematical symbol that only works on the left side of the equals. The simplest one is the remainder of a division. For example if I told you that I had a remainder of 5 after dividing by 20, you wouldn’t know if the original numerator was 25, 45, 65, 85, and so on. This operator is called

mod(modulus). Even if you don’t know what value I started with, It’s not hard to guess what possible numerators could be with modulus. That’s where the cryptography comes into play: a cryptographic hash is designed so that it’s practically impossible to guess the original numerator. We’ll stick with the modulus for explanatory purposes, but imagine that you can’t list off possible numerators like I did.Now we can invent a puzzle for a computer to solve. We’ll start off with the same values as before, but - again - we are disallowing easy guesses. This forces us to check

1 mod 20,2 mod 20,3 mod 20,4 mod 20,5 mod 20and so on. Eventually we’ll hit25 mod 20giving us the solution toX mod 20 = 25. Now you can go back to the person that gave you the puzzle and prove that you’ve done 25 steps of work to arrive at a solution (or have made a lucky 1/25 guess). This is called “proof of work”. A cryptographic has consists of a certain number of bits, such as 256 bits - this means a series of 1’ s and 0’s 256 long. The puzzle presented to the computer is “find the numerator that results in the first 50 bits being zero” (the more bits are required to be zero, the longer it will take to find the answer). Because of the incredibly slim chance of guessing the correct numerator, it doesn’t really matter if the computer counts up (like we did with modulus) or guesses. So, in practice, everybody trying to find the solution starts at a random number and starts counting, or trying other random numbers, until someone wins the jackpot. It’s basically a lottery, but the correct numbers have to be discovered instead of being dropped out of a glass ball at the end of the week. Once a computer finds a solution, everybody else playing the game can check their numerator as [probabilistic] proof that they have done work.Now we can use this lottery to create a blockchain. We start with 5 things: a globally agreed on solution we are looking for (789), an initial block (which is just a number - lets say 12345), Bob’s account #5 of $100, and Sally’s account #6 of $200, and a huge amount of players of the above game. Sally wants to transfer $20 to Bob, so she says to all the players: “I’m #6 and want to give #5 $20. There’s a $1 prize for finding a new block for me.” All the players make a new denominator, by placing the numbers next to eachother - so

12345 6 200 5 100 20 1- or just1234562005100201. All the players start trying to find the number that will result in 789. Eventually someone finds 1234562005100990 after a lot of work/guesses. Everybody checks their work1234562005100990 mod 1234562005100201 = 789. The winning player receives their prize, and now everybody has a new block to start from:1234562005100201 1234562005100990. Next time someone wants to send some money they will use12345620051002011234562005100990as the initial block instead of 12345. Hence, we have set up a chain starting with:12345->12345620051002011234562005100990-> …There’s your block…chain. Anybody can independently verify that the work has been done by checking the answers. It’s incredibly elegant but, as we’ve seen, incredibly destructive.

Blockchain is often described as a solution in search for a problem. It’s a clever technology, but people don’t really know what it can be used for besides storing cryptocurrency transactions.

People have thought about storing other kinds of data in the blockchain, like health records, but no one can really point out to why this would be better than other solutions.

To achieve something similar with health records without blockchain, all that is needed is just a cryptographic signature. The hospital cryptographically signs a digital health document and email it to you. The hospital in turn stores it in some shared database accessible by other hospitals. Done.

If the health record is somehow lost from the shared database, then you got your own copy of it as backup. They can’t modify the health record either, because then it would diverge from your own copy.

The worst thing they can do is to add falsified health records without your approval, but that’s a problem with blockchain as well. Blockchain cannot verify that the input data is truthful (garbage in, garbage out).

The cryptographic signature step is a part of blockchain either way, so there’s no extra technical overhead in the non-blockchain way.

Even if a particular coin has a finite number of possible coins, it exists in an unbounded universe of other coins.

Can someone tell me how decentralized money became the enemy? It is decentralized currency that is like everything we stand for literally using mastodon protocol here.

it’s not the creators fault that the first thing the userbase did was centralize it onto these marketplaces lol. I’m reminding people that this is conceptually great but terrible implementation, across the board.

Ok but the Fossil version control system (which uses a mini-blockchain to store software version history) is pretty cool

I think it’s funny how most lemmy users are pro open source, pro privacy, pro digital rights; but once it comes to money all that is thrown out of the window and they happily get on their knees for paypal and the few other large players.

Yes, the current state of crypto is a mess. People are attracted by the promise of the big payout, rather then seeking an alternative payment system, making them ripe for scammers that promise the world, but in the end only rug “investors”. Even “functional” cryptos are often highly centralized, making them as bad as banks in terms of reliability. Almost none implement any privacy features, and if they do, its typically a tacked on afterthought.

But this does not make the original idea invalid. Will it ever live up to the promise of alternative money? Maybe. Maybe not. Only time will tell if the issues that exist right now will be fixed.

If making payments in crypto back to FIAT was free it would be more popular. For me it’s mostly useless since the fee to spend crypto is more than the (often free) fee for using my credit card.

New needs to be better and cheaper to be picked up.

In my experience it works extremely well for everything online and digital content. The instance I’m on? 100% crowd funded with microdonations and the hoster directly accepts it without conversion back to fiat. I pay my email and VPN also like this, and on mullvad you even get a 10% discount.

But yes, for everything physical it’s a long way ahead to become widely accepted.

There’s attempts at having payments with 0 fees, that is, if you don’t involve exchanges or payment service providers, who obviously charge a fee for fiat conversion.

Using Nano you have 0 fees for the transaction and ideally as little as 0.25% fee at an exchange for fiat conversion.

It’s not only without fees, it’s very fast (ideallly sub-second confirmation) and eco-friendly (requiring no special hardware, because there is no mining and using very little energy overall).

What’s lacking is places where you can actually pay for things with Nano, but that’s the classic chicken and egg problem.It would also be popular if the entire crypto landscape wasn’t replete with late stage capitalist-douche tech bros trying to scam literally everyone.

Just because it’s open source doesn’t mean it’s good. Also not every situation is the same. Using Linux instead of windows has advantages/disadvantages very different than using crypto instead of fiat.

I can think of thousands of reasons to pick Linux, thousands to pick windows and thousands to pick fiat. I’d have to think real hard to even think of a single reason to pick crypto over fiat.

I prefer free software not for its price, but for the freedom it gives me. Naturally I donate to these causes roughly what I’d have spend on a commercial one. They however do not need to know who I am, so I exclusively use crypto for that. I made one exception for an organization using paypal, and promptly they pulled address and name from that, gave it to a 3rd party which then send a postcard to me. You could see it as a nice gesture, but I think it’s just rude to use data in ways I did not explicitly consented to. Just take your money and leave me in peace.

In a similar manner I like to use it to pay for email, vpn, hosting and other online stuff. In fact this lemmy instance is 100% paid for by microdonations from its users, and because the provider accepts it directly no conversion was needed.

but once it comes to money all that is thrown out of the window and they happily get on their knees for paypal and the few other large players.

I don’t think anybody likes paypal, Visa, Mastercard or any of the other major players. It’s just that blockchain “currencies” are much, much worse.

The idea of “Alternative Money” is a silly idea. Money has always been, and will always be connected to a state. The taxing and spending of the state is what gives money its value.

With cryptocurrencies, the “value” is only “greater fool” value. Someone is willing to pay 70k in dollars for a bitcoin because they think someone else is going to be willing to buy it from them for $71k at some point in the future. If it were a legitimate currency people wouldn’t bother checking its value in dollars because it would be useful in its own right. The only legitimate demand for cryptocurrencies is to pay ransom, and even then, the people who get the ransom immediately transform it back to a useful “fiat” currency.

Lemmy users are knowledgeable about open source, privacy, digital rights and knowledgeable enough to know that cryptocurrencies are a scam.

The idea that money is tied to the state is silly. Many things have been used as money, way before the concept of a “state” existed. Undeniably the money that lasted best across the passage of time is gold. Up until very recently it was the standard to settle cross country currency exchanges with. The value does not come from the state, but from people willing to exchange it for goods and services. Todays fiat money is created at will by a few select people that are not democratically elected. They get to decide how much they debase your savings for the “greater good”, while the ones that profit the most are those who control the source.

Most people do not care about their open source, privacy and digital rights, so they only hear and care about crypto when the price jumps or when it is used for crime. Everything else is simply not newsworthy. So you end up with a bunch of “investors” looking to make a quick buck and people who believe to solve crime with more laws (requesting ransoms is already illegal, has existed before crypto and currently gift cards are scammers favorite form of payment).

I never mentioned the price nor suggested investing, because quite frankly, I don’t care. What I do care about is giving the few big companies that control the internet as little data and influence as possible, and not processing payments through them is a really important step. So I keep about as much crypto as I keep cash in my wallet, and use it preferably when buying or selling.

The idea that money is tied to the state is silly.

No, it’s not. It’s historically accurate. All money is state money, always has been, always will be.

Many things have been used as money, way before the concept of a “state” existed.

Nope. Sorry, that’s wrong.

Undeniably the money that lasted best across the passage of time is gold.

Gold isn’t money. Gold is a commodity. Gold was used for jewelry, and as a bright shiny thing that didn’t tarnish had value because of that. People would sometimes exchange gold or things made of gold, but not gold coins. But, they’d also exchange other useful things: food, tools, cloth, etc. Gold coins were created by various states.

people willing to exchange it for goods and services

Never happened. Sure, there were gifts or donations, but it wasn’t X amount of gold for Y amount of grain. There were debts, but debts weren’t listed as a certain amount of gold, or a certain amount of money. Debts are old, money is new. Trading one thing for a certain “price” didn’t happen until coins existed, and coins didn’t exist until there was a state.

Todays fiat money is created at will by a few select people that are not democratically elected

Oh, blah blah blah. “Fiat money” is the only kind of money that has ever existed or will ever exist. It doesn’t much matter whether the government is “democratically elected” or not, currencies are created by and backed by a state and their ability to obtain a monopoly on the use of force within their area of influence. Most states with currencies are currently democratic, even if the structure of the US federal reserve is confusing to you.

They get to decide how much they debase your savings for the “greater good”, while the ones that profit the most are those who control the source.

More blah blah blah crypto nonsense.

Look, do some research on this stuff. Debt is a good place to start.

people willing to exchange it for goods and services Never happened.

This is literally what you do every day. You exchange something for goods and services. This something is money based on it’s functional role, not some obscure definitions. To be money, it must be used as money. To be used as money, a group of people must agree that the item is worth exchanging for. This something does need to fulfill additional properties to be useful, notably it must be fungible, durable, portable, recognizable, divisible and have a stable supply. Gold does fit this description, but so does fiat.

What you are describing is a government issued currency, which has some overlap with money, but is not the same thing. Maybe you should research on this stuff.

This is literally what you do every day. You exchange something for goods and services

Yes, now that there’s money it’s what happens. Prior to money there were debts, but no exchange of “X” for a set amount of goods or services.

To be money, it must be used as money.

To be money it must meet all the definitions of money. It must be a store of value, it must be a unit of account and a medium of exchange. There was no real money until there were states.

What you are describing is a government issued currency

Government issued currencies are the only real currencies. Everything else is valued by what someone will pay for it in government issued currency.

Gold being a commodity because its shiny and therefore has value is no different than “I want to use this coin to better protect my data and privacy”. Both are values attributed to a commodity. Also, “It may have intrinsic value (commodity money), or be legally exchangeable for something with intrinsic value (representative money), or only have nominal value (fiat money).”

https://en.m.wikipedia.org/wiki/History_of_money

You are wrong that money has always existed as state issued. That isn’t true

Gold being a commodity because its shiny and therefore has value is no different than “I want to use this coin to better protect my data and privacy”.

It’s completely different. Gold is a commodity because it is inherently useful in itself. If someone invented a way to create gold out of thin air, people would continue to want gold because it’s pretty and shiny, and because it’s a very good electrical conductor that doesn’t tarnish. Crypto coins are only useful because everyone thinks that a greater fool will come along and pay as much or more. Everyone knows they have no inherent value, but so far there has always been a greater fool.

You are wrong that money has always existed as state issued. That isn’t true

Sure it is.

Hey by the way, after we had that discussion bitcoin surpassed silver to become the 8th most valuable asset by market cap on the entire planet More than coca cola and Pepsi combined.

Also no, money has existed outside of States and Countries before you should look into the Theory of Money and the history behind it

Crypto is a liberterian capitalist’s wet dream.

Tax-free, anonymous, with no accountability. Perfect for white washing corporate gain.

Just because it is “open-source” doesn’t mean it will be used for good.

Wait until you hear about cash! We should outlaw that immediately.

Crypto is not anonymous. Even monero, the most private cryptocurrency, has a feature called “view only wallets”, so 3rd party auditing is possible, if not easier then auditing today. Will individuals use it to avoid some taxes? Sure, it gets easier for them. Will corporations avoid more taxes then they already do? Doubtful.

A view only wallet doesn’t trace anything that doesn’t get received directly by that view only wallet. If we had two wallets that didn’t interact with that wallet, it couldn’t do shit to trace or audit my transactions.

If you are a company and run a webstore, it could be mandatory that all funds must go through a wallet where the tax authorities have a view key. This would be trivial to enforce with penalties whenever for publicly using addresses that point to other wallets. Peer to peer transactions (for eg. used goods or produce from your garden) are already except from taxes in my jurisdiction, so these transactions can be private.

Ahhhh I see what you mean now that’s true but would be dependant on the legislation of the area like you said.

This is what I learnt on Lemmy. Not all people who agree with your position have arrived there logically. (In my case, this position would be leftist ideals). People who you share the same values with are not exempt from being illogical.

New tech leads to scammers pouncing on it to make a quick buck. However, just because scammers pounce on it doesn’t make the tech bad inherently.

See Lemmy’s hate for AI for instance. The advancements in the field of machine learning are mind boggling. Lemmings unfortunately fail to disassociate the tech from the scammers who talk about this tech. It’s disappointing, but oh well… ¯\_(ツ)_/¯

AI has the potential to become a tool which strongly favors and benefits the ruling class. Us peasants get the locked down version, while government agencies get to use the full power for cyber warfare and disinformation campaigns, and large corpos get to manipulate (“advertise”) to you in most manipulative way to act in their best interest.

The way I see it good people shy away form using AI, leaving only the assholes wielding their new would powers. Those with ill intentions will find ways to use it, no matter how many laws you put up to prevent it. To defend yourself the best approach would be to learn how to use AI yourself, so that you can detect and react when AI is used against your best interests.